尽管铂金在2025年飙升了127%,但即使价格出现如此显著的上涨,世界铂金投资理事会(WPIC)的展望仍显示市场将持续多年处于短缺状态。我是爱德华·斯特克(Edward Sterck,WPIC研究总监),世界铂金投资理事会(WPIC)的研究总监。大宗商品市场经济规律表明,解决供应短缺的一个途径是价格上涨,以激励更多供应进入市场或抑制需求。然而,即使我们已经看到价格大幅上涨,WPIC仍预测未来市场将出现显著短缺。今天与我一同讨论的是WPIC的首席分析师韦德·纳皮尔(Wade Napier),他将解释为何在价格走高的情况下,我们仍预测会出现这些持续多年的短缺。我们今天讨论的重点显然将是基本的供需基本面,但同样重要的是要认识到,我们目前所处的环境是地缘政治和宏观经济因素对铂金市场价值产生巨大影响的环境。暂且将这些因素放在一边,专注于基本面,让我们来看看二至五年的展望。

爱德华·斯特克:韦德,根据WPIC的展望,未来五年铂金市场的大局是怎样的?

韦德·纳皮尔:我认为未来五年铂金市场的大局,是巩固过去三年我们经历的严重短缺状态。我们预计2026年市场将实现平衡,然后从2027年到2030年将再次出现更多短缺。

爱德华·斯特克:很好。这显然是作为一系列长期研究的一部分发布在世界铂金投资理事会网站上的。但你提到这里有一些变化。与我们之前的展望相比,发生了什么变化?

韦德·纳皮尔:最大的变化,正如你所提到的,实际上是价格。2025年价格上涨了127%,而随着价格上涨,供应市场的意愿也随之增强。因此,我们将未来五年的供应预测上调了约1.3%。价格上涨会降低消费铂金的倾向,因此我们将未来五年的总需求预测下调了约1.9%。供应增加和需求减少的净效应是,我们的年均市场短缺量已从大约每年50万盎司减少到约每年35万盎司。

爱德华·斯特克:但是,尽管短缺略有减少,我的意思是明确地说,这些仍然是相当可观的短缺。

韦德·纳皮尔:当然,平均而言,它们约占年度需求的4%。

爱德华·斯特克:谢谢,韦德。那么简单回顾一下,供需平衡显示2023、2024和2025年每年都出现短缺,但2026年市场将达到平衡,然后再次出现短缺。2026年的市场平衡意味着什么?我的意思是,这当然应该表明我们看到当前市场紧张状况会有所缓解吧?

韦德·纳皮尔:不一定。最终,市场平衡意味着需求等于供应。因此,如果2025年市场紧张导致摩擦和价格上涨动力,那么在2026年,即使需求等于供应,同样的市场紧张状况可能依然存在。

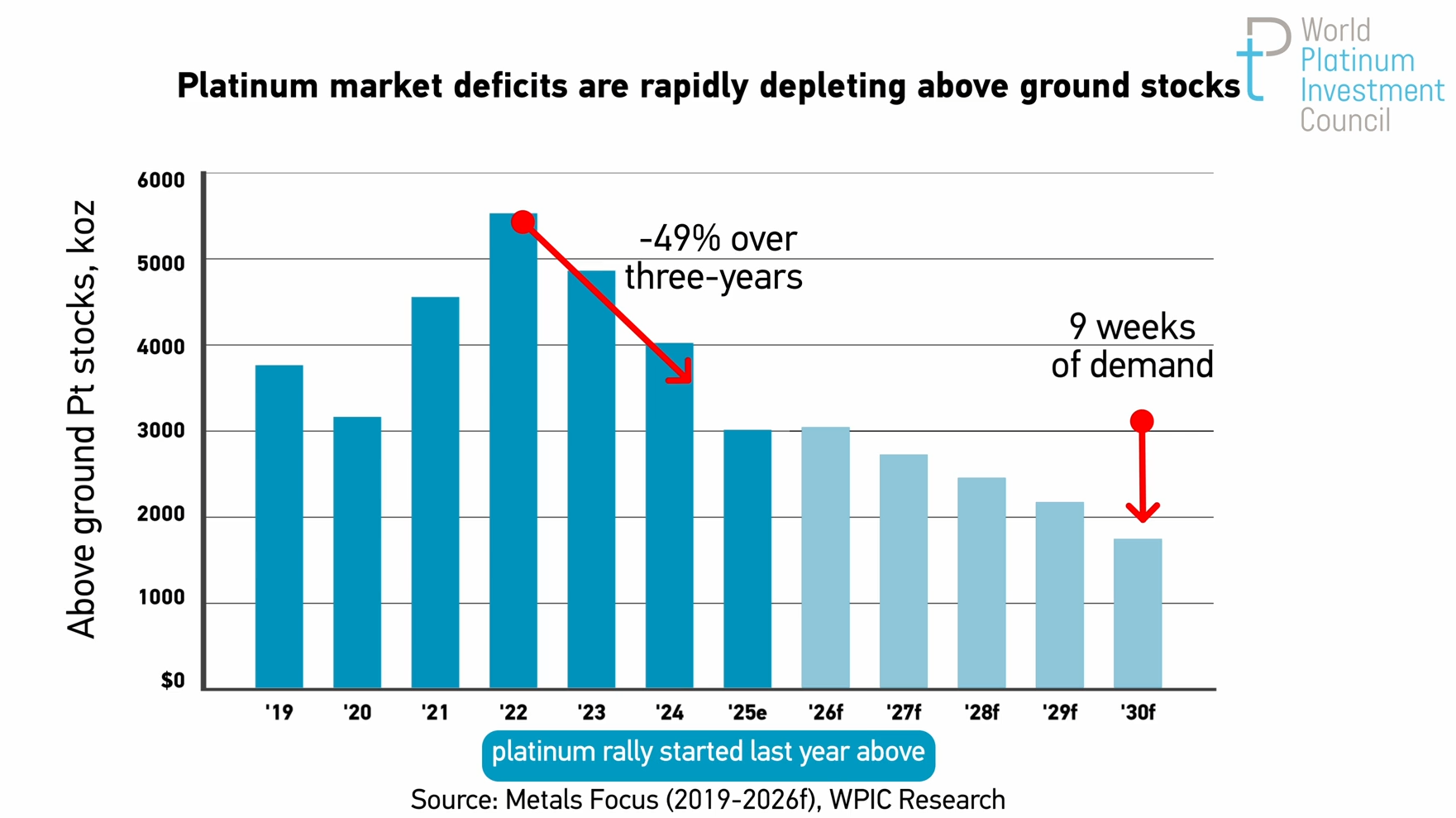

爱德华·斯特克:所以实际上,你知道,出现市场短缺时,短缺是通过消耗地上库存来弥补的。我们实际上要表达的是,去年铂金价格上涨开始时,地上库存已经消耗到了不可持续的低水平。但2026年的市场平衡并不会以任何方式重建这些地上库存。

韦德·纳皮尔:是的,不会补充地上库存。

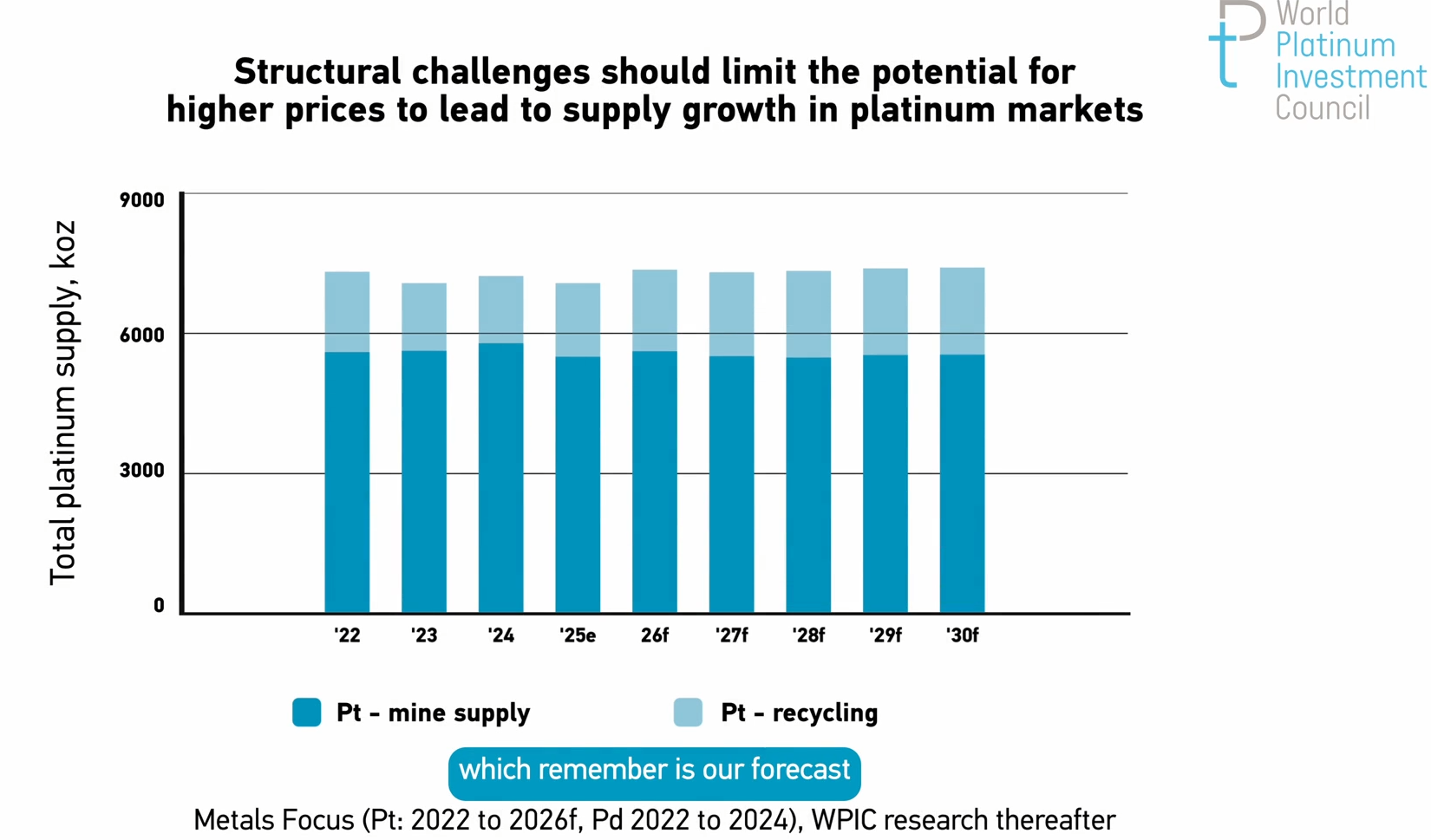

爱德华·斯特克:谢谢。那么,让我们更详细地关注一下价格上涨带来的后果,先从供应端开始。价格上涨肯定对矿山经济效益有积极影响。那么,矿业公司为何不采取行动试图增加供应,以获取更多经济上行潜力呢?

韦德·纳皮尔:你说得完全正确,爱德。更高的价格确实能改善经济效益。然而,采矿业的现实是,无论是资本、劳动力还是资源,都高度密集。当我们考虑到从勘探过程、经济研究过程、建设过程到产量爬坡过程,从头到尾可能需要10到12年的时间。因此,尽管去年价格上涨,但实际上要在未来五年内(请记住这是我们的预测期)大幅增加供应,是非常困难且极不可能的。这就是为什么我们看到在我们的预测期内,矿山供应基本保持稳定。

爱德华·斯特克:我想这里需要记住的一个关键点是,这些都是深层地下矿井。因此,它们本质上缺乏灵活性,需要挖掘大型竖井,而且在我们今年的供需预测中,只有一个新项目投产,而该项目是10年前开始建设的。

韦德·纳皮尔:是的,那就是铂谷矿山(PlatrFeef mine)。

爱德华·斯特克:提醒一下,当然,在我们的矿山供应展望中,我们只采用生产商指引的汇总中点值。我们实际上并未在此之上加入自己主观的覆盖预测。

韦德·纳皮尔:是的,我们使用公司的指引。

爱德华·斯特克:谢谢。那么换个角度,但继续谈供应,看看回收供应,预测显示未来五年回收供应预计将增长18%。为什么回收供应会因价格上涨而增加,但我们却没说矿山供应也会以同样方式增加?

韦德·纳皮尔:正如我提到的,矿山供应对价格相当缺乏弹性,而回收供应则更具价格弹性。我们拥有成熟的回收收集价值链,这些链条能够更快地对价格做出反应。然而,在过去大约三年左右价格相对低迷的时期,我们并未看到那些回收量出现。这并不是说那些催化剂没有被收集。所以现在随着更具激励性的价格出现,我们预计其中一部分量将会释放出来。因此,当我们考虑我们预测的铂金回收供应增长18%时,实际上其中很大一部分是前置的。

爱德华·斯特克:很好。现在先把供应放在一边,转向需求。看看预测,尽管价格上涨,但在五年时间范围内,需求实际上预计将大致保持平稳。这看起来相当有韧性,毕竟价格实际上翻了一番还多。这种韧性背后是什么原因?你能为我们梳理一下从汽车、工业、珠宝到投资需求等不同需求类别的情况吗?

韦德·纳皮尔:正如你所说,是汽车、工业、珠宝和投资需求。汽车需求通常是最大的,约占年度需求的30%到40%。在这里我们认为,销售内燃机汽车或混合动力汽车发动机,仍然需要在汽车催化剂中使用铂族金属(PGMs),而这种需求将会有很长的尾部效应。工业需求方面,铂族金属是化工综合设施、玻璃制造厂或石油炼化厂总成本中的一小部分。因此,同样地,铂族金属价格不一定会对这些行业的整体大局产生重大影响。珠宝是一个确实能看到一些价格弹性的领域,因为消费者的可自由支配支出会受到铂金价格上涨的影响。因此,在我们五年展望中,我们将珠宝需求预测下调了约7%。投资需求是所有细分领域中最不稳定的。我们采取的做法基本上是延续过去十年的需求模式以保持一致性。

爱德华·斯特克:我猜,总结一下需求对价格实际上缺乏弹性的原因,我们所说的就是,在大多数情况下,要么你必须使用铂族金属,因为法规从排放角度要求你这么做;要么,根本不存在可行的替代品;要么,使用铂族金属的成本效益实际上超过了其成本。

韦德·纳皮尔:完全正确。

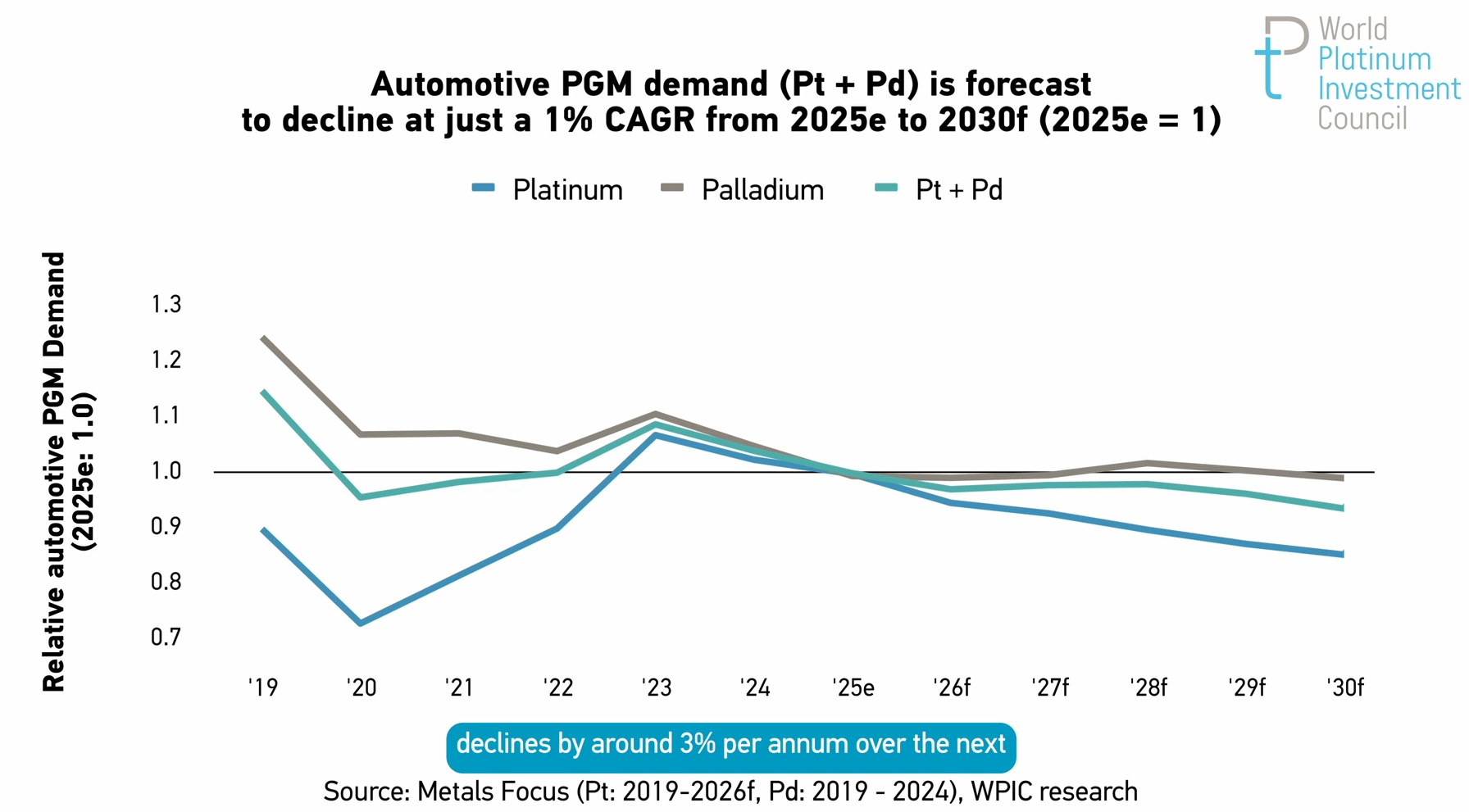

爱德华·斯特克:那么让我们更深入地探讨一下汽车行业的前景。几年前可能有些人说过,到2030年我们都会开特斯拉。显然,更多的电动汽车意味着混合动力或纯内燃机汽车(ICE)会减少。这对铂族金属的前景意味着什么?

韦德·纳皮尔:我认为电动汽车领域的前景确实已经发生了变化。我们看到了一些法规上的回退,最近是2025年在欧洲和美国,电动汽车的目标被降低了。这意味着内燃机汽车和混合动力汽车可能比之前预想的会保持更高的市场份额。话虽如此,在我们五年的预测期内,我们仍然预计电动汽车市场份额会增长,从目前的约16%-17%增加到2030年售出的新车中约有28%是纯电动汽车。

爱德华·斯特克:那替代呢?我的意思是,考虑到催化转化器,里面通常有三种不同的铂族金属:铂、钯、铑。在某种程度上,金属负载量之间存在一定的灵活性,特别是在铂和钯之间。鉴于过去八九个月左右铂和钯的价格上涨,这有什么影响?这在预测汽车需求方面如何影响我们的展望?

韦德·纳皮尔:它们肯定会产生影响,因为现在铂金相对于钯金建立了每盎司约三四百美元的溢价,我们预计一些铂金汽车需求将被钯金需求所替代。因此,当我们观察我们对铂金的独立汽车需求预测时,我们认为未来五年铂金汽车需求每年下降约3%,而钯金汽车需求,由于受益于从铂金替代而来,预计每年仅下降约0.5%至1%。因此,以铂金加钯金的总和为基础,汽车需求每年应下降约1.5%。

爱德华·斯特克:谢谢。那么在工业需求方面,我是说,我看预测显示前景大体稳定,未来有什么可能改变这一点吗?

韦德·纳皮尔:对于工业需求,我认为“稳定”可能是正确的词,也许会有一些轻微增长,但未来最大的变化或增量将是氢经济的普及。从这个意义上说,我们预计大规模的需求要到2030年或进入2030年代才会真正出现。

爱德华·斯特克:谢谢。最后在需求方面,看看黄金以及黄金对铂金市场可能产生的影响。显然,黄金价格上涨的时间比我们在其他贵金属上看到的要长得多。但也许我们可以从黄金市场吸取一些经验教训,并将其应用于铂金。那么,更高的黄金价格对珠宝需求产生了什么影响?这又如何传导至投资需求?我们对铂金能抱有同样的期待吗?

韦德·纳皮尔:随着过去三四年金价持续走强,我们看到2024年和2025年黄金珠宝需求每年减少了约20%。因此,我们可能会在铂金上看到类似情况。就像我说的,我们已经将未来五年铂金珠宝需求预测下调了约7%。并且我们可能预期看到铂金投资需求的增长。在中国,我们看到金条和金币的需求持续强劲。而交易所交易基金(ETF)则是一个有趣的故事,尽管预期可能出现获利了结,但其需求仍表现出一定的韧性。

爱德华·斯特克:是的,我想这或许值得一提,就是随着价格上涨,你可能会预期出现你提到的获利了结,但实际上我们看到了一些温和的积累。

韦德·纳皮尔:是的,确实如此。我认为显然投资者认识到了铂金具有吸引力的投资理由:供应增长有限、需求稳健,并且市场处于根深蒂固的短缺状态。

爱德华·斯特克:那么结束之前,关于需求的最后一个问题。你提到黄金珠宝需求在高价格下下降了20%以上,但在铂金方面,我们的预测仅下降7%。铂金市场,特别是珠宝市场,与黄金相比有何不同?

韦德·纳皮尔:我认为我们看到铂金珠宝与黄金珠宝的区别在于,铂金珠宝的购买可自由支配度较低。它通常与订婚和婚礼相关。并且它更多地用于镶嵌宝石的珠宝,这是珠宝市场的高端部分,我们预计这部分对更高的价格更具弹性或需求更具韧性。

爱德华·斯特克:那么我们即将结束WPIC的供需展望。你有什么关键要点想与大家分享?

韦德·纳皮尔:我认为这个展望很大程度上是一个巩固期。我们经历了三年的严重短缺,并因此看到了价格支撑的出现。地上库存预计不会得到补充。不仅如此,未来五年,它们将进一步下降,这将巩固我们已经看到的紧张市场状况。

爱德华·斯特克:总结一下,铂金市场在结构上依然紧张。强劲的供需基本面支撑着市场。与此同时,我们面临着高度不确定的宏观政治和宏观经济环境,这对整个贵金属板块构成支撑。当然,这也带来了很大的波动性,投资者应予以注意。那么,今天就到这里,感谢您今天的参与。

原文

Platinum surged 127% in 2025, yet even with that significant price increase, WPIC's outlook is still for multi-year deficit. My name is Edward Sterck(Director of Research, WPIC), I'm the Director of Research at the World Platinum Investment Council, or WPIC. Commodity market economic dictate that one way solve for a deficit is for an increase in pricing, to either incentivise more supply into the market or to disincentivise demand. Yet even with the significant price increase we've seen, WPIC is still forecasting significant market deficits going forward. Joining me today is Wade Napier, WPIC's lead analyst, to explain why we're still forecasting these multi-year deficits despite the higher price. The focus of our discussion today is obviously going to be on underlying supply demand fundamentals, but it's also important to recognise that we're living in an environment where geopolitical and macroeconomic considerations are having an outsized impact on platinum market value. Putting that to one side and focusing on the fundamenrtals, let's turn to the two to five year outlook.

Edward Sterck: Wade, what is the big picture for platinum over the next five years according to the WPIC outlook?

Wade Napier: I think the big picture for platinum over the next five years is consolidating in the last three years where we had substantial deficits. We expect a balanced market in 2026 and then more deficits from 2027 through to 2030.

Edward Sterck: Excellent, and this is obviously published as part of Fa long-term series of research that's available on the World Platinum Investment Council's website. But you mentioned that there are some changes here. What's changed versus our previous outlook? Well the biggest change is, as you alluded to, actually price. So the price was up 127% in 2025 and with that increased price becomes an increased willingness to supply the market. And we have therefore adjusted our supply forecast by about 1.3% higher over the next five years. With the increased price there's less propensity to consume platinum, so we've decreased our total demand forecast by about 1.9% over the next five years. The net effect of that higher supply and less demand is that our average market deficits have been reduced from about 500000 ounces per annum to around 350000 ounces per annum.

Edward Sterck: But whilst they're slightly reduced, I mean to be clear, these are still quite considerable deficits.

Wade Napier: Certainly, on average, they're around 4% of annual demand.

Edward Sterck: Thank you, Wade. And so just to recap, the supply demand balances show deficits in each of the years, 2023, 2024 and 2025. But a balanced market in 2026 before returning to deficits, what are the implications for a balanced market in 2026? I mean, surely that should suggest that we see some easing of the current market tightness

Wade Napier: Not necessarily. Ultimately a balanced market is one where demand equals supply. So in 2025 if you had tight markets that caused friction and upward price momentum, in 2026 if demand equals supply that same market tightness is likely to still be there.

Edward Sterck: So in effect, you know, with a market deficit, that market deficit is satisfied by a drawdown of above ground stocks. And effectively what we're saying is that when the platinum rally started last year above ground stocks were depleted to unsustainably low levels. But the balanced market in 2026 doesn't do anything to in any way rebuild those above ground stocks.

Wade Napier: No, no replenishment of above ground stocks.

Edward Sterck: Thank you. So let's kind of focus in on the consequences of that price increase in a little bit more detail and starting with supply. Surely the price increase is positive for mine economics. So why aren't the mining companies taking action to try and increase supply to capture more of that economimc upside potential?

Wade Napier: Well you're absolutely right, Ed. Higher prices does improve the economics. However, the reality of mining is it's very intensive, whether that's capital, labour or just resource intensive. So when we think about you've got the exploration process, you've got the economic study process, you've got the construction process and then you've got the ramp up process. From start to finish you're looking at potentially 10 to 12 years. And so whilst prices have run last year, in reality to actually increase supply substantially in the next five years, which remember is our forecast horizons, very difficult and very unlikely. And that's why we see mine supply largely stable within our forecast period.

Edward Sterck: And I guess one of the key things to remember here is that these are deep level underground mines. So inherently they're not flexible, you've got big shafts to sink and we've got only one new project coming through in our supply demand forecast this year and that started construction 10 years ago.

Wade Napier: Yes, that's the Platreef mine.

Edward Sterck: And as a reminder, of course, in terms of our mine supply outlook, we are only using the aggregated midpoint of producer guidance. We're not actually putting our own subjective overlay onto this.

Wade Napier: Yes, we use company guidance.

Edward Sterck: Thank you. So kind of taking a turn but continuing with supply and looking at recycling supply, within the forecast that's expected to increase by 18% over the next five years. Why the increase to recycling supply on the back of higher prices, but we're not saying that in same way with mine supply?

Wade Napier: So as I alluded to, mine supply is quite price inelastic, whereas recycling is more price elastic. What you have is well established recycling collection value chains and these are able to more quickly respond to prices. However, in the last sort of three years or so where prices were somewhat depressed, we didn't see those recycling volumes come through. That's not to say that those catalysts weren't collected. So now with more incentive pricing available, we expect some of those volumes to come through. And so when we think about the 18% increase in platinum recycling supply that we forecast, a lot of that's actually front loaded.

Edward Sterck: Excellent. Let's put supply to one side now, turn to demand. Looking at the forecasts, demand is actually expected to remain broadly flat over the five year time horizon, despite the price increase. That seems really quite resilient, despite pricing more than doubling effectively. You know, what's behind that resilience and can you run us through the different demand categories from automotive, industrial and jewellery through to investment demand?

Wade Napier: As you said, it's automotive, industrial, jewellery and investment. So automotive is typically the largest, accounting for about 30% to 40% of annual demand. Here we sort of see that to sell a combustion engine vehicle or a hybrid vehicle engine, you still need PGMs in the autocatalyst and that demand is going to have a long tail. Industrail demand, PGMs are a small component of the total cost of a chemicals complex or a glass manufacturing facility or a petroleum refinery plant. So again, PGM prices won't necessarily have a big impact on the bigger picture in those industries. Jewellery is a segment where we do see some price elasticity, given consumer discretionary spend will be impacted by higher platinum prices. So we have revised our jewellery demand forecast down by around 7% within our five year outlook. Investment demand is the most volatile of all segments. What we simply do is we roll our last 10 years of demand forward to sort of keep things consistent.

Edward Sterck: And I guess so the kind of summarising the demand inelasticity to price effectively, what we're saying is, for the most part, either you have to use PGMs because regulations require you to from an emissions perspective, or, there simply isn't a viable alternative, or the cost benefits using PGMs just outweigh the costs effectively.

Wade Napier: Absolutely.

Edward Sterck: So let's drill in a bit more into the automotive outlook. Some people might have said a few years ago that we're all going to be driving Teslas by 2030. Clearly, more electric vehicles equals fewer in either hybrid or pure ICE (internal combustion vehicles). What does that mean in terms of the outlook for PGMs?

Wade Napier: I think the outlook for the electric vehicle landscape has certainly sort of shifted. We've seen sort of a regulatory rollback, most recently in Europe and the United Stated in 2025, where electric vehicle targets have been watered down. And so the implication is that ICE vehicles and hybrid vehicles are likely to retain a higher market share than previously thought. That being said, within our sort of five year forecast, we still expect electric vehicles to gain market share from a current sort of 16% to 17% to around 28% of new vehicles sold in 2030 will be full electric.

Edward Sterck: And what about substition?I mean if you think about the catalytic converter, you've usually got three different platinum group metals in there, platinum,palladium, rhodium. And now to a degree, there's an element, there's some flexibility between the metals in terms of loadings, particularly between platinum and palladium. With the price increases we've seen for platinum and palladium over the last eight, nine months or so, what are the implications? How does that feed through into the outlook in terms of forecasting automotive demand?

Wade Napier: They certainly feed in the sense that with platinum now establishing a sort of three to four hundred dollar per ounce, price premium over palladium, we expect some platinum automotive demand to be substituted for palladium demand. So when we look at our sort of individual automotive demand forecast for platinum. We think that platinum automotive demand declines by around 3% per annum over the next five years, whereas palladium automotive demand, because it's benefiting from substitution away from platinum, is only expected to decline by about 0.5% to 1% per annum. So on a combined platinum plus palladium basis, automotive demand should decline by around 1.5% per year.

Edward Sterck:Thank you. And then just in terms of industrial demand, I mean, I looking at the forecasts are broadly stable outlook, anything that might change that there in the future?

Wade Napier: For industrial demand, I think stable is probably the right word, maybe some slight growth, but the big change or delta going forward will be the uptake of the hydrogen economy. In that sense, we only really see large demand coming through 2030 or into the 2030s.

Edward Sterck: Thank you. And then just finishing up on demand and looking at gold and the influence that gold can have on the platinum markets. Clearly gold prices have been increasing for quite a bit longer than we've seen in the other precious metals. But perhaps there are some learnings we can take from the gold market, therefore, and apply them to platinum. So what were the impacts of higher gold prices on jewellery demand? How did that feed through into investment demand? And can we expect the same for platinum?

Wade Napier: So with gold prices going from strength to strength over the last three to four years, what we've sort of seen is a reduction in gold jewellery demand by around 20% per annum in 2024 and 2025. And so we could see similarities occur in platinum. Like I said, we have reduced our platinum jewellery demand forecast by around 7% over the next five years. And we could expect to see platinum investment demand growth. In China, we continue to see demand go from strength to strength for bars and coins. While ETFs has been an interesting story where demand has been somewhat resilient despite expectations for potential profit taking.

Edward Sterck: Yeah, and I guess that's something that's probably just worth commenting on is that with the price increase, you might expect that profit taking that you mentioned, but actually we've seen in fact some modest accumulations.

Wade Napier: Yes, certainly. I think it's clearly investors are cognisant of platinum's compelling investment case where you've got limited supply growth, robust demand and a market very much in entrenched sort of shortfalls.

Edward Sterck: So one last question on demand before wrapping this up. You mentioned in terms of gold jewellery demand, 20% plus decrease on higher prices, but in platinum our forecasts are only for a 7% decrease. What differentiates the platinum markets, jewellery market versus gold?

Wade Napier: I think the way we see platinum jewellery versus gold is that there's less discretionary platinum jewellery purchases. It's typically associated with engagememts and weddings. And it also goes into more gem set jewellery, which is the higher end of the jewellery market, which we expect to be more price resilient or demand resilient to higher prices.

Edward Sterck: So we're just wrapping up the WPIC supply demand outlook. What's your key takeaway that you want to share with people?

Wade Napier: I think the outlook is very much one of consolidation. We've had three years of significant deficits where we've seen price support come through. Above ground stocks are not expected to replenish. If anything, over the next five years, they will fall further and this will consolidate the tight markets that we've already been seeing.

Edward Sterck: So just to wrap things up, the platinum market remains structurally tight. You've got the strong underlying supply demand fundamentals. And at the same time, we've got this macropolitical macroeconomic environment with a high degree of uncertainty that's supportive for the precious metals complex of a whole. Of course, that also brings in a lot of volatility, which investors should be aware of. So with that, thank you for with us today.